January was a unique and interesting month for my portfolio. Two big things happened: 1.) two of my holdings were exchanged for their Class B siblings, which I’ll explain in more detail below and 2.) I had my largest Dividend/Coupon payments ever. In this post, I’ll share more detail into my specific holdings.

First lets cover the not so fun stuff, expenses. I owed $5 for the ability to use Robinhood Gold and owed $116 in interest to Robinhood for using leverage through the billing period. At this point, my core holdings are not using this leverage. I am using Robinhood’s leverage to swing trade and to pull funds out to pay the monthly borrowing payments. I owed $394 this month to my credit cards and another $2,431 on my personal loan. In total my portfolio cost me $2,946 in January.

Now for the upside, my swing trading netted me $1,832 this month. I buy and sell ETN’s as well as some other dividend paying stocks. I never sell at a loss, never. If I get caught in a down swing in price, I simply hold and collect the dividends until the price comes back up. This has happened a few times over the last year. The hardest part about swing trading is remaining emotionless. I try to get in and get out in the same day, known as day trading. I don’t try to hit home runs where the prices goes up significantly and that’s when I cash out, but I usually set a target to make between $50-$150 per trade.

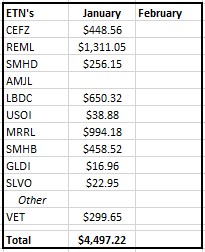

As mentioned in my second point above, I made the most I’ve ever made in a month in coupons/dividends. In January I was paid $4,497! This came from 9 ETN’s and one common stock, VET. This was one of those trades I was holding until it came back up in price so I didn’t take a loss. I was paid $300 just for holding this stock through the ex-dividend date which was the end of December. I later sold in January for a profit as well!! Of the ETN’s one of them only pays each quarter, LBDC. so every 3 months my payouts overall are bigger. Here’s a table of the income in January:

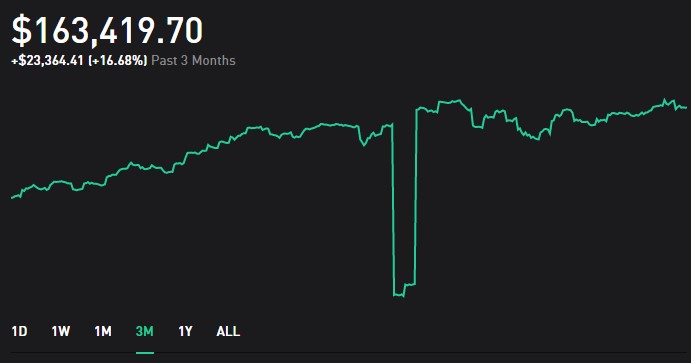

Another unique action that took place in January was an exchange of ETN’s. I had two Series A ETN’s in which UBS currently has a voluntary exchange happening. We have the option to trade our Series A ETN’s for Series B which are essentially the same notes. I was invested in CEFL & BDCL which are part of the exchange. There was a 2 day period in which my current holding were frozen while the exchange of notes was taking place. My portfolio showed a temporary $44k decline. See picture below for what my portfolio did during that exchange period.

As noted in my previous post, https://kittleinvestments.com/what-are-etns/ ETN’s are a unique asset class that needs to be watched closely. Another ETN, SMHD will be redeemed later this year. I will need to make a decision on what to do with this note in the next few months. If redeemed at the current price, I will receive $2.56 per share less than what I paid representing a $2,600 loss. I problem I now get to solve.

Stay tuned for my February ETN high leveraged portfolio update. I’ll also start posting about my peer to peer lending investments soon.

Be Awesome!